Solving For Inflation

Critical Thoughts: Bursting The Bubble of Traditional Inflation Narratives

This is ‘Think: Deeper’, a deep and academic look at issues facing the economy and society with the goal of advancing critical thought in the face of overly simplistic media narration.

Citations have been provided for all sources, with a full list provided at the bottom, along with annotations for each of the sources.

This text is not intended to be political. However, American economics are highly politicized. Mythical beliefs in capitalism are quite common. Unfortunately, this superstitious belief in cosmological capitalism has derailed and distracted from proper debate on modern economic theory. The topic of inflation has been weaponized, and must be seen for what it is, rather than what it is feared to be.

THE INFLATION FOOTHOLD

Rising inflation has emerged as a striking feature of the pandemic-era economy. Contrary to the prevailing view among policymakers and perpetuated by the media, which attributes inflation to "excessive government spending," the actual issue stems from the breakdown of supply chains. The true danger lies not in inflation, but in stagflation.

In the fevered dreams of mainstream fiscal conservative pundits, inflation is pure evil. Inflation goes against the near-religious belief in property rights that “keep civilized society together”. If unemployment scares and a potential return of the Great Depression were what influenced the postwar period of growth and stability (also known as the “Golden Age of Capitalism”), then it was inflation paranoia that characterized the world economy since the crisis of the 1970’s, called “The Great Inflation”.

For these traditionalist thinkers, it’s the combination of state power and “the excesses of democracy” (defined as the rule of the majority, which includes demands for higher spending) that are a great threat to Western civilization, and American corporate power. According to the “great thinkers” of neoliberal (not to be confused with progressive or liberal) thought, this problem should be dealt with at its root.

Individuals such as Milton Friedman desired a Central Bank accountable to no-one, that only followed monetary rules with the primary goal of “taming inflation”1. Then we have Friedrich Hayek, also praised as a “genius” and “great thinker”, and one of the clergymen of conservative economics, who wanted to privatize money itself. The followers of this school of thought believe markets should “impose limits on the demands of the masses.”2

These arguably obsolete ideas still thrive at the highest levels of our land, where a belief in the gold standard, balancing the budget through fiscal policy amendments, and private/digital currencies like Bitcoin are considered clever “fixes for the problems of modern society”. Limitations on democratic participation, specifically where minorities are influential, are also accepted as canon on the right. With soaring inflation during the economic crisis following the pandemic, in which we still find ourselves, it should come as no surprise that government action is the main cause of conservative consternation and public condemnation. It’s noteworthy that the fiscal rescue packages, designed to keep the economy afloat, are the primary target of their ire.

The potential resurfacing of Keynesian ideas is a Friedman-quoting pundit’s worst nightmare. Pushing fears about inflation are a narrative tool for dismantling any plans to improve social spending, and these traditionalist intellectuals believe they can put “an end” to public spending with inflation rhetoric. While many do see it as a necessary consequence of the pandemic, there are many who would not disagree with the conservative diagnosis that a surge in demand, caused by a rapid recovery related to state actions, lie behind inflationary resurgence. The result of these views is reflected in decades of depressed wages for the majority of Americans, with soaring wealth for a select few.3

Some progressive economists believe the real cause of inflationary pressures lies behind a large and ubiquitous corporate movement with vast oligopolistic powers, who have increased profit margins during the pandemic. If concentrated corporate power is the true culprit behind accelerating inflation in the alternative discourse, then rather than cutting back on spending, stabilizing would necessitate the regulation of monopolies and the introduction of price controls. This is basic economic, fiscal, and monetary theory.

Both views tend to accept that demand-pull inflation, and an increase in demand vs. supply, lie at the heart of the problem. For conservatives, workers who are allowed to stay home and receive benefits without working are the source of this demand increase. This is typical, and something that justifies all mythical views about “welfare queens” in conservative folklore. For progressives, the same demand from workers, who are helped by the government through unfairly difficult circumstances, are at the heart of the problem.

However, they are not necessarily to blame, as it is the oligopolistic corporations that create scarcities in supply and raise prices to enrich the true beneficiaries of price increases: wealthy stockholders and CEOs.4 One doesn’t need to be an especially astute observer of economic realities to understand that the real threats to social stability are in fact excessive corporate power and income and wealth inequality, not the expansion of government welfare. This does not mean that inflation is the result of corporate malfeasance, or that regulation, which is certainly needed, would be a panacea for price stability. The prevailing oligopolistic view of inflation, and at least the orthodox viewpoint, misses the role of cost-push inflation. Worryingly, it also disregards in its entirety the role of distributive conflicts that lie at the heart of heterodox views of inflationary processes.5

The rigorous debate between those who focus on cost-push factors and those who’ve championed demand-pull forces has an important history in economics, which can trace its lineage all the way back to the beginnings of this field of study, and back to the debate about inflation in England during the Napoleonic Wars. The serious matter of class conflict, which is central to comprehending inflationary processes, wasn’t properly understood until considerably later.

Works by Joan Robinson, a longtime and well-known disciple of Keynes who may be a key author in the development of progressive or heterodox economics during the postwar era, was central in developing the conflict theory of inflation. This view believes in determining whether inflation accelerates or not based on the sources and the size of the shock, whether it is demand or supply-related, and how these issues can be tackled. More importantly, it considers the social and institutional conditions related to class conflict.

To what extent we’re seeing a resurgence in class upheaval, the first of it’s kind since the 1970’s is, clearly, a question that needs to be answered. While many would like to template this as simply a do-over of the 1970’s, it’s important to discuss the lineage and genealogy of inflationary theory, as well as the reasons for inflation acceleration in the 1970’s and the decades of price stability that followed.

BULLIONISTS, ANTI-BULLIONISTS, GERMANS, AND ALLIES

Historically, periods of inflation were periods of expansion of the global economy. Economic historians concerned with the longue durée argue that there were at least four price revolutions in the West: one tied to the revival of trade routes after the Crusades in the thirteenth century, one after the discovery of the Americas and the opening of the trade route around Africa with Asia in the sixteenth century, one during the Industrial Revolution in the eighteenth century, and one with the expansion of the Industrial Revolution beyond its core in the twentieth century.6 These were prolonged periods of moderate inflation associated with significant transformations of the real economy.

By the sixteenth century, a version of what would be called the quantity theory of money (QTM), which would eventually become the banner of Friedman and the monetarists of the Chicago school, was relatively well established. In the view of its proponents, inflation resulted from the increase in circulation of metallic money, often associated with a new discovery of precious metals like the silver from American mines. Adam Smith and other classical authors rejected this view. For them, the increase in monetary supply did not explain higher prices. Higher prices resulted from changes in real activities — for example, bad crops creating higher prices for foodstuff and increasing the costs of production. The banking sector would adapt, providing the bills of exchange (basically paper money) needed for the functioning of the economy. This view was called the real bills doctrine (RBD), in which the bills needed for the functioning of the economy adjust endogenously to real changes in production, and it can be seen as the opposite of the QTM.7

It is worth noting that the Bank of England (BoE), arguably the first central bank, was founded in 1694 not to control the quantity of money or manage inflation but explicitly to finance the expansionist policies of the crown.8 By 1797, the international crisis initiated by the French Revolution forced the BoE to make the pound inconvertible and allow it to fluctuate against gold. Convertibility would only be fully reestablished in 1821. David Ricardo, the main inheritor of the classical doctrines of Smith, suggested that the period’s inflation resulted from the overissuing of paper currency by the BoE. He endorsed the famous Report of the Bullion Committee of 1810, which recommended a return to the gold standard. The Ricardian view, which saw bank policies in the context of the budgetary needs of war as inflation’s main cause, was known as the Bullionist school. It is still, in some ways, the basis for conventional views on inflation.

The anti-Bullionist position was taken by, among others, Thomas Tooke, who essentially defended the RBD perspective, suggesting that inflation had been caused by a combination of bad crops and higher import prices resulting from the Napoleonic embargo that made importation of grain from the continent considerably difficult. Higher costs of production, and not excessive demand caused by monetary policy, were at the heart of the inflationary process for Tooke. Even though Ricardo’s views, as noted by Keynes, dominated England as completely as the Holy Inquisition conquered Spain, the conventional wisdom now is that Tooke and the anti-Bullionists were basically correct.9

If the Bullionist controversy marked the understanding about inflationary processes within the economics profession, it was the German hyperinflation of 1923 that created almost all the myths about inflation that still plague debate about the topic. German hyperinflation followed the defeat in World War I and the infamous Treaty of Versailles, heavily criticized by Keynes, that burdened the Weimar Republic with an unsustainable amount of debt in foreign currency. According to the Allies trying to collect the reparations, the inflationary process resulted from the excessive spending of the German government and the overissuing of money by the Reichsbank — a position accepted by Keynes, whose views on inflation remained relatively conventional throughout his life. The Germans, not surprisingly, disagreed. Karl Helfferich, who had been finance minister during the war and who was one of the main leaders of the German balance of payments school, argued that the cause of hyperinflation was the need to pay for reparations in dollars. (It wasn’t only Germany that owed money to the United States; the web of inter-allied debts forced France and the United Kingdom to pay back their obligations in dollars, too.) In their view, the need to depreciate domestic currency to make exports more competitive and obtain dollars for the repayment of reparations caused hyperinflation.

While reviewing a classic book on German hyperinflation that described the Allied and German views, The Economics of Inflation by Costantino Bresciani-Turroni, Robinson noted that both views were incomplete and that an analysis of the role of the distributive conflict was needed to provide a full explanation of the events. For her, “neither exchange depreciation nor a budget deficit can account for inflation by itself. But if the rise in money wages is brought into the story, the part which each plays can be clearly seen.”10 In other words, German hyperinflation was triggered by depreciation and higher import prices, but it was the resistance of workers, whose real wages had declined as a result of the higher prices of imported goods, that created the conditions for an inflationary crisis. Higher wages implied further increases in prices and the need for more depreciation, since German exports lost competitiveness with higher costs of production. A wage-price spiral followed, and inflation, resulting from the distributive conflict, got completely out of control.11

Inflation is not just about shocks to demand and/or supply that lead to higher prices but about sustained processes that create the conditions for a persistent increase in price level. At the root of the problem are the social norms of what is acceptable for different groups and the deep-seated historically and institutionally grounded questions of the bargaining power of those groups. Inflation, in this heterodox framework, is about the distributive conflict.12

FROM GREAT INFLATION TO GREAT MODERATION

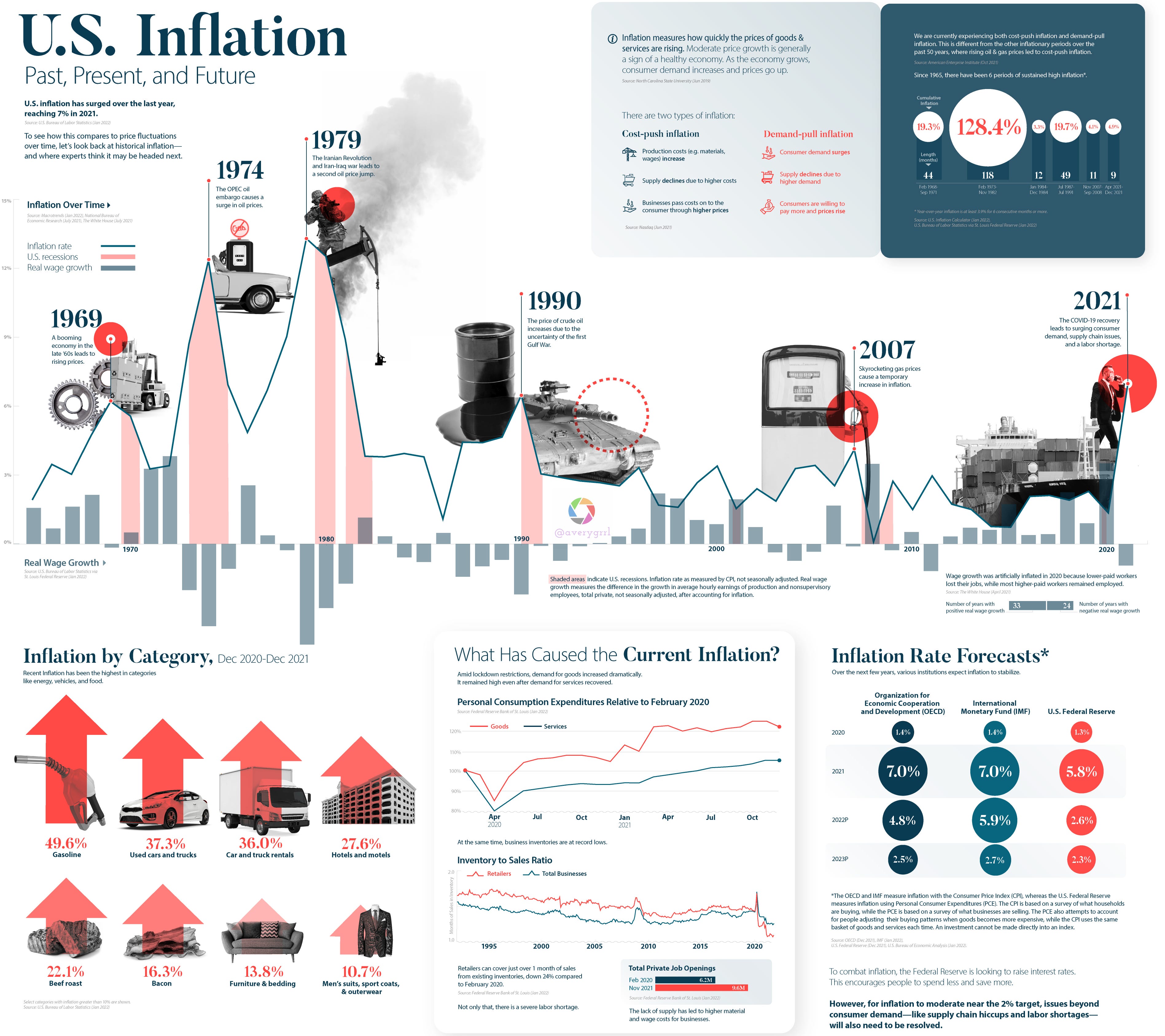

The decades that followed World War II were not only associated with relatively rapid rates of output growth but also with fairly stable prices. The long period of price stability, at least in advanced economies, reflected an implicit social agreement. The macroeconomic environment that emphasized the maintenance of full employment, and the social legislation that protected workers’ rights within the context of the expansion of the welfare state, strengthened the power of trade unions. However, the Keynesian consensus implied that wages would only increase at the same pace as productivity gains, maintaining inflation under control. In other words, the reductions in costs associated with increasing productivity were not reflected in lower prices or in higher gains for corporations but were essentially passed on as wages. This was an economy in which prices had floors but no ceilings, in Robert Heilbroner’s apt expression, something clearly visible in the data since the 1940s, when deflationary periods almost vanished (Figure 1).13

Figure 1. Inflation Rate (1866-2021)

This policy consensus, which began to collapse in the 1960s and was completely shattered by the 1970s, was only possible in the context of the Cold War.14 It is important to emphasize that in the United States, the welfare state was incomplete, with women and minorities excluded from many of the civil and political rights taken for granted in the so-called free societies. The reasons for the collapse of the Keynesian consensus are associated with what Christopher Lasch would call the revolt of the elites, and can be seen as part of the Polanyian “double movement,” according to which those social groups that lost out with the rise of the Golden Age led a backlash against it.15 But as the consensus that provided the social and institutional basis for economic prosperity was collapsing, the militancy of the working class and other social pressure groups was at its pinnacle. One of the fundamental consequences of the Golden Age’s demise was the Great Inflation of the 1970s.

The conventional view about the acceleration of inflation emphasizes the role of the Vietnam War, mostly its fiscal costs, and the expansion of welfare programs during the Lyndon B. Johnson administration, including the War on Poverty and the extension of medical benefits to the elderly and the poor. Many would blame the lax monetary policies of Arthur F. Burns, a relatively orthodox economist appointed by Richard Nixon to head the Federal Reserve. Friedman’s view on the monetary causes of inflation seemed vindicated, and he received the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel, legitimizing that opinion. Nobody would deny the importance of the two oil shocks, in 1973 and 1979, in explaining the acceleration of inflation, but the orthodox argument certainly became the accepted view about inflation’s fundamental causes.16 Even before the victory of Ronald Reagan in 1980, which finally brought the radical right to power with an explicit critique of the Keynesian consensus, Democrats had accepted the orthodox view of inflation and implemented its policies. Jimmy Carter appointed Paul Volcker, a monetarist and an inflation hawk, as chairman of the Fed.

Volcker initially tried monetary targets as prescribed by Friedman, and later, as the policies of explicitly managing the money supply failed, the Fed switched to the more conventional hikes of its policy interest rate.17 The Volcker interest rate shock was part of a set of policies that brought inflation down, even if their effects were not necessarily the ones anticipated by orthodox economists. Stabilization was not the result of lower monetary emissions so much as the fact that significantly higher interest rates, and the recession that followed, together with the opening of the American economy to foreign competition (in particular East Asian economies with lower wages), led to a large increase in unemployment and a decrease in the bargaining power of trade unions. Deregulation, which also started with Democrats under Carter and accelerated under Reagan, provided a further blow to the position of the working class. In addition, a steady decline of commodities prices, particularly oil, in the 1980s was instrumental for achieving price stability. Volcker is seen in orthodox circles and in the mainstream media as having promoted the stabilization, along with what the more recent chairman of the Fed Ben Bernanke called the Great Moderation, the long period of price stability that followed the Great Inflation.18 In reality, it was the restraining of workers’ demands and the attenuation of the distributive conflict that mattered.19

To some extent, it was the success of the Golden Age that led to a less combative working class, in particular once the rights of minorities created a wedge in the Democratic coalition and allowed for the rise of right-wing populists like George Wallace and for Nixon’s “Southern strategy.” The new accumulation regime based on trade liberalization, financial deregulation, and the curtailing of workers’ rights was only exacerbated during the Reagan, George H. W. Bush, Bill Clinton, and George W. Bush administrations. And while Barack Obama did expand medical coverage and remains for some a more elusive and harder to classify figure, it is clear that he did not challenge the basis of the new neoliberal consensus that eventually replaced the old Keynesian one of the Golden Age.

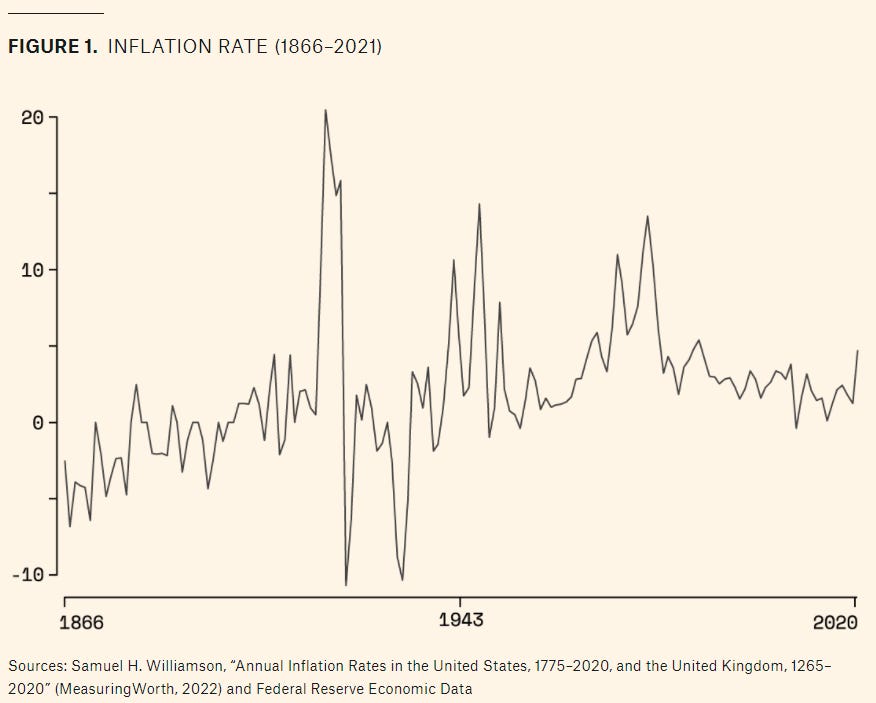

Figure 2. Productivity and Real Compensation in The US (1948-2020)

The neoliberal consensus provided a new social and institutional basis for the process of accumulation, one in which inflation remained subdued. The fundamental difference between the two accumulation regimes can be seen in the relationship between productivity and real compensation of nonsupervisory workers (Figure 2). While real wages increased with productivity in the postwar era, from the 1980s onward there has been a decoupling, with wage stagnation creating the conditions for price stability. During the Keynesian consensus era, productivity grew at around 3 percent per year, while in the neoliberal era, the pace slowed down to about half a percent per year. The slowdown in productivity went hand in hand with lower growth of output and employment. Financial accumulation, rather than real accumulation associated with output growth, became the norm, something referred to as financialization.20 It would take a change to the underlying social conditions that regulate the process of capitalist accumulation and a significant increase in the bargaining power of the working class to lead to a new inflationary crisis.21

The legacy of the Great Moderation and the neoliberal period of deregulation, particularly in financial markets, has been one of increasing instability. As a result of the global financial crisis (GFC) of 2008, with its epicenter in the United States related to the housing market bubble, the Fed was forced to intervene heavily in the economy. A relatively moderate fiscal package was also passed, and a slow and prolonged recovery started during Obama’s administration and continued well into Donald Trump’s. Nobody seriously thought there was any significant risk of the demise of the Great Moderation.22 But then the pandemic hit in late 2019 and early 2020.

THE PANDEMIC AND COST-PUSH INFLATION

The overwhelming preoccupation at the beginning of the COVID-19 pandemic was with precluding a total shutdown of the economy. Vigorous financial rescue plans were implemented, larger than the one after the GFC a decade or so before, suggesting that something was learned from the last crisis. Monetary policy was geared to prevent the collapse of financial institutions and maintain levels of spending, just like in 2008, with the Fed expanding on the already large balance sheet and increasing the money supply even further. In other words, both fiscal and monetary policy were largely expansionary, as has become the norm in recessions going back at least to the postwar era, where the lessons of inaction during the Great Depression were understood.

The shutdown led to an immediate reduction in demand for several sectors, as people stayed home and stopped consuming many goods and services. In addition, significant supply-side effects were felt in sectors that had to shut down, either for lack of consumers or simply because sanitary conditions prohibited continuous production.23 This in turn led to additional supply-side bottlenecks that caused increased costs of production in sectors acutely impacted by the pandemic. The increase in prices was localized to a few sectors: used cars, airfare, restaurants, housing, and, more important, the energy sector, with reductions in production and transmission spreading through the whole economy. Transportation issues, with clogged ports and problems in the trucking industry, added to the inflationary pressures from the cost side. Note that energy and transportation are costs of production for almost everything else, creating economy-wide inflationary pressures. These are temporary shocks, but their persistence depends not only on the ability of supply chains to adapt but also on the end of the pandemic, which is a global problem that will persevere while there are unvaccinated people. If the pandemic persists and the intermittent disruptions become endemic, so will the moderately higher levels of inflation.

It is clear that these cost pressures would have an impact on the economy even if the fiscal and monetary packages had not promoted a recovery in demand. But it is hard to agree with the notion that it was the government’s generous social spending that spawned inflation.24 Orthodox economists like Clinton’s Treasury secretary and Obama’s adviser Larry Summers, who did not seem to have much influence within the White House and the Fed at the beginning of Joe Biden’s administration, are now much more popular within the corridors of power. Summers’s view that fiscal restraint and tighter monetary policy are needed to control inflation has gained some momentum, and Jerome Powell, recently reappointed as chair of the Fed, has already suggested that monetary tightening is on the agenda. However, the notion that the recovery has been extremely fast, defended by Summers and, for obvious reasons, by the White House, is misplaced, and it should be taken with a grain of salt. The recovery has been significant, but the economy has not been close to full employment for a long time, even if the pre-pandemic unemployment rate was low. This is the key issue in the discussion of whether more restraint regarding fiscal and monetary policy is needed or not. If the economy is not at full employment, and the recovery is not caused by excess demand, then contractionary fiscal and monetary policy to curb demand would make little sense.

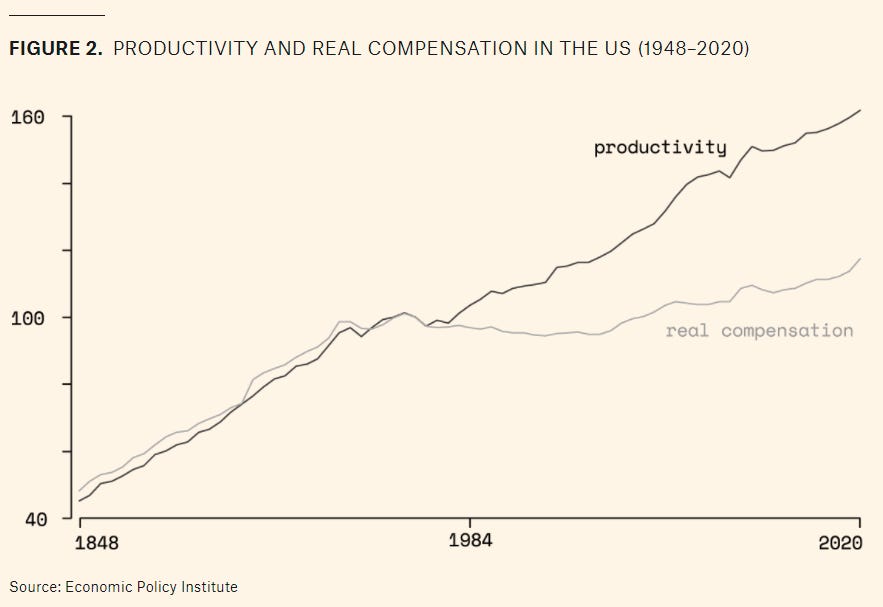

The arguments suggesting that the economy has recovered quickly tend to point to the steep increase in personal consumption after the pandemic, which was possible, even with higher unemployment, as a result of the government’s fiscal transfers. It is true that personal consumption, as a share of gross domestic product (GDP), has recovered fast, as shown in Figure 3. Stimulus checks and child tax credits, both of which allowed for sustained consumption, together with restrictions on evictions and temporary increases in the Supplemental Nutrition Assistance Program (SNAP), promoted a large decrease in poverty.25 This increase in consumption suggests that demand was repressed, but it does not imply that the economy is at its capacity limit.

FIGURE 3. PERSONAL CONSUMPTION AND GROSS DOMESTIC INVESTMENT (% GDP)

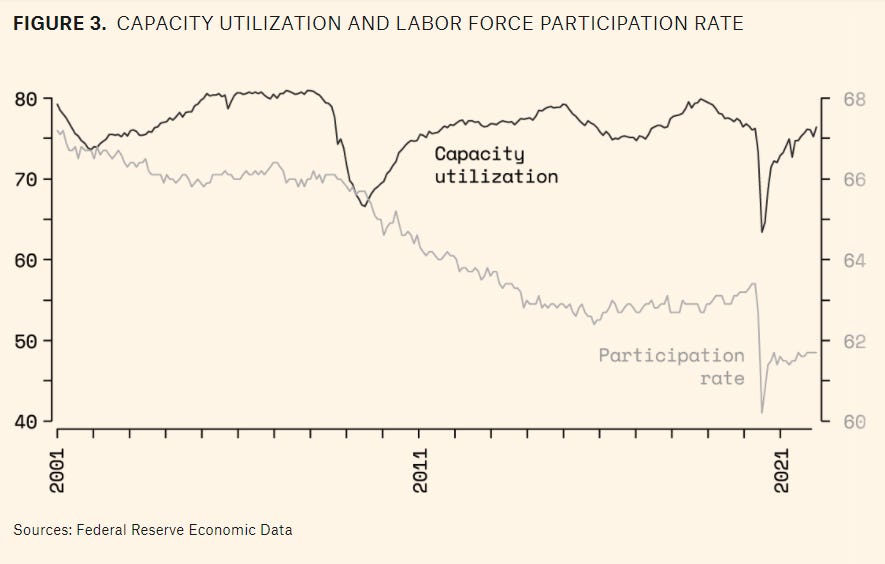

FIGURE 4. CAPACITY UTILIZATION AND LABOR FORCE PARTICIPATION RATE

Give the poor some additional money, and they will consume. The question, then, is whether firms can provide for that demand and whether they are investing in order to increase production capacity. As can be seen in Figure 3, gross domestic investment, as a share of GDP, has recovered, but it has not increased significantly. In fact, capacity utilization remains relatively low, below pre-pandemic levels and below the levels of the previous early 2000s boom (Figure 4), suggesting that lack of growth, and possibly secular stagnation, as Summers described it before, are still relevant concerns.26 Labor force participation rates have been low for years, having peaked at the end of the Clinton administration more than two decades ago, as can be seen in Figure 4. Employment will take a while to return to its pre-pandemic levels, and depending on the ability to sustain the current levels of spending, that would perhaps happen only by the end of 2022.

All in all, the economy still shows signs of slack rather than being at full capacity. Average hourly earnings of production and nonsupervisory employees (i.e., workers’ wages) have grown faster during the pandemic, even if below 1970s levels, and more in sectors that were hit harder by sanitary measures, like leisure and hospitality. Employers are finding it harder to hire workers, too. But that reflects workers’ ability to avoid dangerous health situations or to cope with child-rearing issues and other family circumstances as a result of the fiscal transfers, rather than a labor market that is close to full employment. There were about 3.5 million more workers employed in March 2020 than in December 2021. Irrespective of the official definition of a recession, the economy cannot seriously be thought to have recovered before employment levels surpass the previous peak. All these reinforce the notion that inflation is caused by cost-push factors related to the supply chain shocks, and that these may be somewhat persistent, to the extent that the pandemic endures. The current risk is not one of accelerating inflation but one of persistent stagnation and lukewarm growth with moderate inflation. In other words, it might be called stagflation.

THE DANGERS OF INFLATION PARANOIA

The danger of stagflation does not imply a return of the relatively high inflation of the 1970s, in part because workers are less organized now and it is unclear that significant wage resistance is possible. In this new Gilded Age, with extreme corporate power, workers are not positioned to push for higher wages. The neoliberal branch of the Democratic Party went along, grudgingly, with the Biden fiscal transfers and the infrastructure plan, but it managed to stall and most likely kill the vast majority of progressive programs in the Build Back Better initiative, given the refusal of senators Joe Manchin and Kyrsten Sinema to pass it without Republican votes. Several pandemic programs that have been essential for the recovery — for maintaining the levels of demand and for reducing poverty rates — have ended or are about to expire. Even if it is unlikely that the Fed can increase its policy rate significantly, simply because doing so would likely throw the economy into a tailspin, moderate increases might have an impact on the housing market and slow down the recovery.

For neoliberal progressives, the persistence of inflation makes the risks of contractionary policy a necessary evil. As they accept the conventional story about the Great Inflation, they have bitterly decried the use of price controls that some progressives, as noted before, have defended,27 suggesting that they failed back then and would not work now.28 Price controls worked sometimes, though, under certain circumstances. For example, during World War II — when the government had ample ability to intervene and plan what private companies had to produce as part of the war effort — price controls were fairly efficient, as discussed by Isabella Weber in How China Escaped Shock Therapy.29 But it would be an exaggeration to suggest that the relatively moderate inflation of the 1950s up to the late 1960s, other than during the Korean War, was tied to price and wage controls, which were used only sporadically. As noted before, the basis of price stability in the postwar era was the social accord guaranteeing that wages increased with productivity. It was the social and institutional arrangements keeping the distributive conflict under control that did the job. And while it is true that the pandemic and the return of hegemonic disputes between China and the United States implies that a greater degree of control over the supply chain by US corporations is likely, it is unreasonable to assume that the current administration has the tools to implement price controls as effectively as it did back then, or that these could meaningfully reduce inflation pressures.

In the neoliberal era, what has moderated inflationary pressures is the stagnation of wages. Some might think that the rise of Bernie Sanders and progressive Democrats in Congress signals a change in the social conditions underlying the macroeconomic regime of accumulation. It is true that the rise of the socialist left or the return of New Deal liberalism (depending on one’s preferences), more than the resurgence of a violent and militant right, is the fundamental political change of our time in the United States. The populist right has an old pedigree, and a direct line can be traced from Barry Goldwater to Trump.30 (See notes below.) It is also true that this change comes after several popular movements, from Occupy Wall Street to Black Lives Matter, that urge a radical reform of the current economic system and its social forms of domination. These movements demand higher wages, a Green New Deal, unionization (e.g., at Amazon and successfully at Starbucks), broader and tighter regulation of corporate power, and better working conditions more generally. Inflation was not on their agenda, even if it clearly impinges on their demands. But the danger for the Left, and for the current administration, is to accept an exaggerated estimation of the social evils of moderate inflation.31

The political economy of inflation suggests that if the administration goes for tighter fiscal policy, and the Fed complements it with even slightly less expansive monetary policy, one can expect not just a defeat in the next midterm elections but a full-fledged return of right-wing populism, with Trump or someone like him winning the presidency in 2024. James Galbraith correctly pointed out that it was not inflation per se that caused Carter’s political defeat and the rise of Reaganism, but the way in which the government responded to it.32 Tighter budgets and higher interest rates, which have dominated anti-inflationary policy ever since Volcker, led to twelve years of Republican rule. This might be a repeat of the 1970s — this time, not as a tragedy but as a farce.

Notes/Sources:

In modern versions of this theory, the central bank would control inflation by managing the interest rate, maintaining inflation around a target of 2 percent per year. That target has been modified in the United States to an average target over a period of years, with inflation possibly being higher in some years. For the statement about the new policy goals, see Federal Reserve, “2020 Statement on Longer-Run Goals and Monetary Policy Strategy” (2020).

Constitutional limits on the ability of the government to run budget deficits were also part of the neoliberal program to contain the growth of the Leviathan and avoid another inflationary crisis. James M. Buchanan, of the Virginia school, was keen to tie up the hands of self-interested politicians and impose legal limits on public spending. See Nancy MacLean, Democracy in Chains: The Deep History of the Radical Right’s Stealth Plan for America (New York: Penguin, 2017).

Both Paul Krugman and Larry Summers have suggested similar views. The former sees inflation as a necessary evil, while the latter, perhaps more in line with what Nancy Fraser has referred to as “progressive neoliberalism” when discussing Bill Clinton’s New Democrats (Fraser, “From Progressive Neoliberalism to Trump — and Beyond,” American Affairs 1, no. 4 [2017]), sees inflation as an indication of the need to curtail fiscal spending. In Krugman’s view, the main distinction between the two camps is that one sees inflation as transitory while the other sees it as permanent and requiring more drastic action. See Krugman, “The Year of Inflation Infamy,” New York Times, December 16, 2021; Summers, “The Fed’s Words Still Don’t Measure up to the Challenge of Inflation,” Washington Post, December 16, 2021.

For a recent exposition of this view, see Stephanie Kelton, who argues that “Companies with enough market power can also unilaterally raise prices in a quest for greater and greater profits” (Kelton, The Deficit Myth: Modern Monetary Theory and the Birth of the People’s Economy [New York: Public Affairs, 2020], 47). A similar argument was put forward by Isabella Weber in the context of the pandemic (Weber, “Could Strategic Price Controls Help Fight Inflation?” Guardian, December 29, 2021). Progressive views emphasize supply-side problems, but only to suggest that “large corporations with market power have used supply problems as an opportunity to increase prices and scoop windfall profits.” Corporations are not constrained so much as they use supply problems, creating unnecessary scarcity as a tool to obtain extra gains. As such, it is not the supply constraint in action but rather that oligopolistic firms, faced with expanding demand, can increase prices before the capacity limit is truly reached. This view echoes the language used by Jen Psaki, White House press secretary, blaming greedy corporations for inflation (Jeanna Smialek, “Democrats Blast Corporate Profits as Inflation Surges,” New York Times, January 3, 2022).

Orthodox economic views follow the dominant neoclassical paradigm in economics, and essentially believe that markets produce efficient outcomes. Note that many liberals and more than a few progressives are, from an economic point of view, orthodox, and while they believe that markets are efficient in an idealized world, they think that market imperfections are common in reality. Heterodox views of the economy derive from the work of John Maynard Keynes’s disciples at Cambridge, which suggested that markets do not lead to efficient outcomes. See Marc Lavoie, Post-Keynesian Economics: New Foundations (Cheltenham: Edward Elgar, 2014).

Matías Vernengo, “Money and Inflation,” in A Handbook of Alternative Monetary Economics, ed. Philip Arestis and Malcolm Sawyer (Cheltenham: Edward Elgar, 2006).

Roy Green, Classical Theories of Money, Output and Inflation: A Study in Historical Economics (London: Palgrave Macmillan, 1992).

Matías Vernengo, “Kicking Away the Ladder, Too: Inside Central Banks,” Journal of Economic Issues 50, no. 2 (2016).

Lawrence H. Officer, “Bullionist Controversies (Empirical Evidence),” in The New Palgrave Dictionary of Economics, 3rd ed. (New York: Palgrave Macmillan, 2017).

Joan Robinson, “A Review of The Economics of Inflation by Brcould also lead to higher prices, and, with wage resnce, a wage-price spiral could follow. But Robinson, writing in the late 1930s, was well versed in the ideas of the Keynesian Revolution and knew that the economy normally fluctuated at a position below full employment. Similar ideas on the possibility of supply-side shocks, with propagation mechanisms related to incompatible income claims by workers and capitalists, were developed slightly later in Latin America. The Mexican economist Juan Noyola Vázquez noted that the process of development required a change in the structure of production, with a decrease in the share of agriculture. Bottlenecks in the production of foodstuff, together with wage resistance, led to a wage-price spiral and to structural inflation. This was the basis of the so-called structuralist school of thought in Latin America (see Alcino Camara and Matías Vernengo, “Allied, German and Latin Perspectives on Inflation,” in Contemporary Post Keynesian Analysis, ed. L. Randall Wray and Matthew Forstater [Cheltenham: Edward Elgar, 2005]).

For a recent survey of heterodox theories of conflict inflation, see Robert A. Blecker and Mark Setterfield, Heterodox Macroeconomics: Models of Demand, Distribution and Growth [Cheltenham: Edward Elgar, 2019]).

The postbellum period in the late nineteenth century, tied to the rise of the modern oligopolistic corporation and the initially subdued efforts to regulate their power, was a period of deflation, which makes the argument for oligopolistic inflation hard to defend. Friedman, in his classic book on the monetary history of the United States, suggested that deflation was caused by the demonetization of silver, the infamous “crime of 1873,” and that it was resolved by the discovery of gold in South Africa (see Milton Friedman and Anna Jacobson Schwartz, A Monetary History of the United States, 1867–1960 [Princeton: Princeton University Press, 1963]). This was essentially the view of Populist politicians like William Jennings Bryan, and the reason for his famous fight against the gold standard. The reduction of transportation costs, in an age of globalization with a relatively weak labor force, played a more important role in the deflationary pressures of the era.

See Andrew Glyn, Alan Hughes, Alain Lipietz, and Ajit Singh, “The Rise and Fall of the Golden Age,” in The Golden Age of Capitalism: Reinterpreting the Postwar Experience, ed. Stephen A. Marglin and Juliet B. Schor (Oxford: Clarendon Press, 1990).

See Matías Vernengo, “The Consolidation of Dollar Hegemony After the Collapse of Bretton Woods: Bringing Power Back In,” Review of Political Economy 33, no. 4 (2021).

This is not to say that Friedman’s views on the acceleration of inflation should be taken at face value. For a critique of the orthodox view on the acceleration of inflation and the relationship between inflation and unemployment, see James Forder, Macroeconomics and the Phillips Curve Myth (Oxford: Oxford University Press, 2014).

Charles Goodhart noted that every time a central bank tried to control a monetary aggregate, the previously stable relationship between that particular monetary aggregate and economic activity broke down. This became known as Goodhart’s Law. In the 1980s, the relatively stable relation between money supply and prices broke down, and central banks more explicitly moved in the direction of following interest rate policies with explicit inflation targets. For a discussion of the evolution of central banking, see Goodhart, “The Changing Role of Central Banks,” Financial History Review 18, no. 2 (2011).

See Ben Bernanke, “The Great Moderation,” remarks given at the Eastern Economic Association, Washington, DC, February 20, 2004.

Nathan Perry and Nathaniel Cline argue, on the basis of the post-Keynesian and structuralist theories of conflict inflation, that stabilization was due primarily to wage declines and falling import prices caused by international competition and exchange-rate effects (Perry and Cline, “What Caused the Great Inflation Moderation in the US? A Post-Keynesian View,” Review of Keynesian Economics 4, no. 4 [2016]). The view that inflation in the 1970s was not the result of the excesses of the Keynesian state and the overissuing of money supply were broadly shared at that point by more conventional Keynesians. James Tobin, a neoclassical Keynesian and an acerbic critic of Friedman, argued that he was “not sure how to classify the inflations … in [the 1970s]. [He had] been pretty sure that United States inflation was of the inertial species, but [he] would not exclude the possibility that more fundamental social conflict is arising from the frustrations of continued economic reverses” (Tobin, “Diagnosing Inflation: A Taxonomy,” in Development in an Inflationary World, ed. M. June Flanders and Assaf Razin [New York: Academic Press, 1981], 29).

For a discussion of financialization, see Gerald A. Epstein, ed., introduction to Financialization and the World Economy (Cheltenham: Edward Elgar, 2005); and Thomas I. Palley, “Financialization: What It Is and Why It Matters,” Levy Economics Institute, Working Paper no. 525, 2007.

Charles Goodhart and Manoj Pradhan are among the few that argue that inflation will return for structural reasons. However, their argument proceeds along orthodox lines. They suggest that the global slowdown of population growth would lead to higher dependency ratios and more demand, since the young and the elderly consume but do not produce, leading to persistent excess demand and inflation. See Goodhart and Pradhan, The Great Demographic Reversal: Ageing Societies, Waning Inequality, and an Inflation Revival (London: Palgrave Macmillan, 2020).

An exception was Allan Meltzer, who argued that “If President Obama and the Fed continue down their current path, we could see a repeat of those dreadful inflationary years [of the 1970s]” (Meltzer, “Inflation Nation,” New York Times, May 3, 2009).

For an early discussion of whether the pandemic should be seen as a demand or supply shock, see Matías Vernengo and Suranjana Nabar-Bhaduri, “The Economic Consequences of COVID-19: The Great Shutdown and the Rethinking of Economic Policy,” International Journal of Political Economy 49, no. 4 (2020).

Summers suggests that the stimulus packages were so strong that the economy is essentially back to full employment. He argues that if one looks “at what’s happening in the labor market, it looks to me like we’ve got substantial labor shortages that push wages up, but only with a lag because wages aren’t reset constantly” (“Larry Summers Gets His ‘Told You So’ Moment on Inflation,” Bloomberg, December 23, 2021). In other words, the economy recovered, and inflation is demand-driven. Krugman, who thinks we are in the midst of a strong recovery, is less keen about contractionary policies.

The estimates of the reduction of poverty rates as a result of the pandemic stimulus measures are nothing short of shocking. By some estimates, poverty would be reduced by about 67 percent (Laura Wheaton, Linda Giannarelli, and Ilham Dehry, “2021 Poverty Projections: Assessing the Impact of Benefits and Stimulus Measures,” Urban Institute, 2021).

See Lawrence H. Summers, “U.S. Economic Prospects: Secular Stagnation, Hysteresis, and the Zero Lower Bound,” Business Economics 49, no. 2 (2014). On the possibility of persistently lower rates of growth, see also Robert J. Gordon, The Rise and Fall of American Growth: The US Standard of Living Since the Civil War (Princeton: Princeton University Press, 2016).

Kelton, in The Deficit Myth, suggests two basic measures to control inflation. The first is higher taxes that would reduce spending and pressure on the supply of goods and services, but that would seem to be relevant only at full employment. She also defends a job guarantee program that would provide employment to all who wanted to work. This latter mechanism can be seen as a type of incomes policy, trying to reduce wage demands. Kelton briefly cites wage and price controls in a footnote to her discussion of tax increases.

Noah Smith has provided a brief description of orthodox views on why price controls would not work. Essentially, he argued that price controls would create additional imperfections and retard the adjustment of supply chains (Smith, “Why Price Controls Are a Bad Tool for Fighting Inflation,” Noahpinion, January 1, 2022). It is worth noting that Tobin, back in the early 1980s, favored some use of price controls. He said: “We are not going to have a successful disinflation without some kind of wage and price controls. Right now, we are just relying on tight money and on the natural desperation of disaster … to moderate the wage demands of workers, stiffen the backbones of employers and induce price discounting. That will work eventually, but it is a very painful way to do it and very costly to the economy” (Jane Bryant Quinn, “Economist Tobin on Inflation: How It Started, How to Stop It,” Washington Post, November 2, 1981). Those views have increasingly lost support within mainstream Keynesianism.

Isabella Weber, How China Escaped Shock Therapy: The Market Reform Debate (London: Routledge, 2021). John Kenneth Galbraith recounts his experience within the Office of Price Administration during World War II in his book A Theory of Price Control (Cambridge: Harvard University Press, 1952). Hugh Rockoff suggests that price controls were effective in certain periods, essentially from 1942 to 1946, but less so when controls were relaxed. For him, in order to be effective, price controls had to be “backed up by a vigorous enforcement effort and three important supplementary measures — wage controls, the seizure of noncomplying industries, and rationing both of resources and of final products” (Rockoff, Drastic Measures: A History of Wage and Price Controls in the United States [Cambridge: Cambridge University Press, 1984], 108). These additional conditions are hard to replicate in the current circumstances.

It is worth noting that Trump has abandoned some elements that were central to the right-wing coalition, like the defense of free trade, something that is also part of the progressive agenda on the Left.

While inflation paranoia runs high in DC policy circles and in the media, the fact remains that very few can explain the reasons for an inflation target of 2 percent, or even a target of 2 percent over a period of time. A famous study by the World Bank in the 1990s could not find any effect of very high inflation (40 percent per year) on economic growth. See Michael Bruno and William Easterly, “Inflation Crises and Long-Run Growth,” Journal of Monetary Economics 41, no. 1 (1998).

James K. Galbraith, “Whipping Up America’s Inflation Bogeyman,” Project Syndicate, November 19, 2021.

Amazing work, Avery. Thank you.